This portion of the research provides a deeper position on Vietnam edifice stuffs industry with concentration on the recent concern state of affairs of building and edifice stuffs market. Information about edifice stuffs houses is besides provided.

1.1 Construction and existent estate

Vietnam’s economic system has gone through a fighting period of unsubstantial recognition enlargement, because of the decelerated development in the banking system characterized by non-performing loans ( NPLs ) and a belongings market slack. The belongings market in Vietnam is presently disheartened, challenging with market conditions including a deficiency of capital resources have resulted in building companies being unable to complete undertakings, while buyers are happening it disputing to afford belongings because of a deficiency of entree to loans. As a consequence, many building undertakings, lodging, flats, etc. are being unfinished.There are besides marks of hard-pressed belongings assets in the state. Therefore the building industry’s growing rate declined from 19.7 % in 2011 to 6.5 % in 2012, although the industry reached a Compound Annual Growth Rate ( CAGR ) of 19 % from 2008 to 2012 ( Timetric, 2013 ) .

The building market in Vietnam is expected to be higher than mean growing rates until the terminal of the decennary ( CB Richard Ellis Group, 2008 – 2013 ) . Construction disbursement was about US $ 18.6 billion in 2012, which accounted for somewhat under 20 % of the country’s GDP. This disbursement is estimated to turn by about 7 % per one-year over the following five old ages ( Savills, 2013 ) . In Vietnam building market, the residential sector made up the largest proportion of more than half of entire building disbursement in 2012, followed by the substructure sector. The non-residential market constituted merely approximately 10 % of entire building disbursement in 2012. ( IHS Inc. , 2012 )

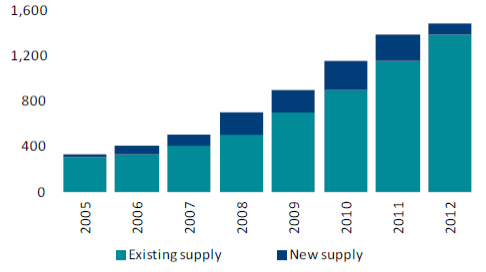

Presently, a mismatch between supply and demand in the Vietnamese belongings market has happened. Demand perseveres for low-cost lodging, office but building developers of mid to high terminal assets are in trouble to pull purchasers or rental consumers. This tabular array showed the bing and the new supply for office market in Vietnam.

Chart 10: Existing and new office supply.

Unit of measurement: sqm ( 000s )( Savills, 2013 )

In Cushman & A ; Wakefield Market mentality 2013, it stated that current mean rents for Grade A in Vietnam have decreased by 46 % and 41 % in HCMC and Hanoi severally, compares to 2008. Meanwhile the entire value of stock list in lodging undertakings was estimated at more than VND125 trillion ( US $ 6 billion ) in 55 metropoliss and states in May 2013. High existent estate monetary values and over-supply, which have rocketed due to bad activities at the extremum of the market, are serious jobs. They resulted in rental rates declined during the recent old ages with mean rents throughout all classs falling by about 2 % quarter-on-quarter ( DTZ Vietnam, 2012 ) . Contractors are keeping on a batch of purchased existent estate merchandises at comparatively high monetary values and are unwilling to sell at a loss monetary value throughout the current downward tendency. In many studies were submitted to building houses and Vietnamese authorities, they all advised to turn to the over-supply issue, accommodations to the flat size and degree of development are necessary.

In Asia Construction Outlook by AECOM in 2013, they forecasted that all major sectors in Vietnam would turn over the following five old ages at similar rates. Specifically, entire building end product of Vietnam would be at around $ 18.5 billion boulder clay 2018, with the growing rate of about 6.7 % . Infrastructure investing, such as main roads, rail and ports, will be a chief growing country until the terminal of the decennary. However, the authorities is likely to hold limited capacity for funding much of this because it is likely to be constrained by public debt degrees. As a consequence Vietnam is set to offer important chances through in private financed substructure undertakings, with the support likely to take the signifier of foreign direct investing or PPP joint ventures. Geographically, the big sum of the investing will be focused on Hanoi, Ho Chi Minh and the North-South corridor in between.

1.2 Constructing stuffs market

1.2.1 Features

The companies

In Vietnam edifice stuffs industry, about top makers are state-owned. See the tabular array 3 and 4 below for the top edifice stuffs house in Vietnam harmonizing to VNR500:

Table 3: Top 12 biggest edifice stuffs houses in Vietnam

| Rank | Company | Type | Merchandises |

| 1 | Ha Tien Cement JSC | State-owned | Cement |

| 2 | Viglacera Corporation | State-owned | Tiles, Building Glass, Sanitary wares, AAC, bricks |

| 3 | Cement Holcim Vietnam | Joint Venture | Cement |

| 4 | Nghi Son Cement | Joint Venture | Cement |

| 5 | Chinfon Cement Corporation | Joint Venture | Cement |

| 6 | Vincem Hoang Thach Co. Ltd | State-owned | Cement |

| 7 | Vincem Bim Son JSC | State-owned | Cement |

| 8 | Vissai Group | Private | Cement |

| 9 | Phuc Son Cement JSC | Joint Venture | Cement |

| 10 | FICO JSC | State-owned | Cement |

| 11 | Phu Tai JSC | Private | Rock, Tiles, Wood |

| 12 | Vincem Hoang Mai JSC | State-owned | Cement |

Note that the joint venture companies above are among state-owned companies and foreign investors.

Table 4: Top 12 biggest private edifice stuffs companies in Vietnam

| Rank | Company | Merchandises | Note |

| 1 | Vissai Group | Cement | |

| 2 | Phu Tai JSC | Rock, Tiles, Wood | |

| 3 | Quangninh building and cement JSC | Cement | Sub-company of SOE |

| 4 | Prime Vinh Phuc Company | Tiles | |

| 5 | Vinh Tuong Industrial Corporation | Ceiling, wallboard grid | |

| 6 | Song Gianh Cement Co. Ltd. | Cement | Sub-company of SOE |

| 7 | Viglacera Ha Long JSC | Terracotta tiles | Sub-company of SOE |

| 8 | DIC Intraco JSC | Steels, AAC, Wood, Roof tiles, Klinkers | Sub-company of SOE |

| 9 | Le Phan Construction Co Ltd | Concrete | |

| 10 | Vicostone | Rock | |

| 11 | Prime Dai Viet JSC | Tiles | |

| 12 | Tay Do Cement JSC | Cement | Sub-company of SOE |

As you can see from the above tabular arraies, the state-owned edifice stuffs companies account for big proportion in the industry. They besides are the ruling factor in private sector, it has created bad concern environment in Vietnam due to inducements that SOEs have received. Therefore, they do non hold really active domestic challengers who put force per unit area on them to introduce.

Sing to types of merchandises, it is seen that cement is the top precedence in the industry. 10 out of 12 biggest makers are bring forthing cement and cement related merchandises. This sector has contributed a big ratio in export activities of Vietnam ( see table 9 ) . However, presents, tiles sector attracts more attending of authorities because of this sector’s importance on the planetary market. Vietnam ceramic tiles sector was ranked in the top 10 states of fabrication and exporting tiles ( Stock, 2010 ) .

1.2.2 Domestic public presentation

As stated in above portion, all 3 chief sectors of building and existent estate ( residential, substructure and non-residential ) has been fighting in the ability to finish their undertakings. Not merely that, the economic crisis led to high rising prices, tightened recognition enlargement, and lower disbursement of people. It made people less likely to purchase, or lease a new house or even repair or upgrade their house. Therefore, the edifice stuffs market of Vietnam has besides suffered a serious downward tendency in development.

Sing ceramic market, harmonizing to studies and articles from Vietnam constructing ceramic association ( VBCA ) in 2013, the sum of manufactured tiles was somewhat under 70 % of entire capacity, estimated around 289.8 million square metre. This figure is much lower than 375 million square metre in 2010 when Vietnam was ranked the 5th on top fabrication states over the universe with 3.9 % on the universe production ( Stock, 2010 ) . Stock of tiles that was hard to unclutter, was about 50 yearss of production, about 40 million square metre or 112.800.000 USD. On the other manus, healthful ware merchandises were produced about 70 % of entire capacity, assessed at 9 million units, and figure of units in stock list hit an norm of 50-60 yearss of production, about 1.2 million units or about 28.200.000 USD.

Table 5: Entire ingestion for tiles and healthful ware of Vietnamese makers.

| 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | ||

| Entire domestic ingestion volume | Tiles( million sqm ) | 150 | 203.65 | 297.5 | 290 | 272 | 246,9 |

| Sanitary ware( million unit ) | 7.5 | 7.8 | 9.0 | 9.7 | 9.3 | 8.5 | |

( Vietnam Ceramic Business Association, 2013 )

As we can see from Table 5, the volume of domestic ingestion for tiles and healthful ware started to diminish significantly from 2011, since Vietnam stand in its ain recession. Before this twelvemonth, the universe economic crisis evidently had no negative effects on the local market because the sum kept raising until 2010.

Table 6: Entire tiles ( ceramic and porcelain ) in stock of some Vietnamese makers

| No. | Company | Max Capacity( million sqm/ twelvemonth ) | Actual Capacity( million sqm ) | In Stock( million sqm ) |

| 1 | Mikado | 1.5 | 1.07 | 0.1 |

| 2 | Viet Y | 1.8 | 1.30 | 0.25 |

| 3 | Granite Trung Do | 3.5 | 2.43 | 0.4 |

| 4 | Prime | 99 | 74 | 5.5 |

| 5 | Catalan | 15 | 10.5 | 1.3 |

| 6 | CMC | 5 | 4 | 0.3 |

| 7 | Vinh Thang | 9 | 6.5 | 0.6 |

| 8 | Vitaly | 4.5 | 2 | 0.3 |

| 9 | Thach Ban | 2 | 1.2 | 0.2 |

| 10 | Toko | 15 | 10.5 | 2 |

| 11 | Viglacera | 25 | 20 | 2 |

( Vietnam Ministry of Construction, 2013 )

From Table 6, it is clearly seen that those 11 maker of tiles in Vietnam did non make the maximal mark capacity of them, and besides had a big measure of tiles in stock which is really hard to unclutter.

Regard to constructing glass merchandises, Vietnam has 7 companies bring forthing over-size edifice glass with maximal capacity is over 150 million square metre. However, in 2012, the goods in stock was about more than 60 million square metre of standard glass. It somewhat equaled 4 month capacity of all makers. Furthermore, in that 60 million, there was 57 million metre of float glass, severally 5 month production end product. Besides that, imported glass from China and ASEAN states with lower monetary value besides impacted on Vietnamese firm’s ingestion. Therefore, some mills had to impermanent halt bring forthing for a piece, for case, Viglacera Dap Cau glass mill was closed from in-between 2012 to September 2013 due to flood.

In 2013, ingestion of bricks and roofing tiles experienced a 70 % of overall capacity. The existent produced measure of brick was estimated of 17 billion units, but the purchased measure merely reached 14 billion bricks, approximately 80 % .

Table 7: Bricks fabricating capacity and ingestion in 2012.

| Merchandise | Maximum Capacity | Actual end product | Consumption |

| Factory criterion brick | 14 billion | 12 billion | 10 billion |

| Manual brick | 6 billion | 5 billion | 4 billion |

| Entire | 20 billion | 17 billion | 14 billion |

Unit of measurement: brick. ( Vietnam Ministry of Construction, 2013 )

A new sort of brick ( or barricade that is non-fired ) which was started to bring forth in Vietnam non long ago, is Autoclave Aerated Concrete ( AAC ) blocks. It besides has been fighting with end product clearance because of low demand in building, particularly no new undertakings tend to implement this sort of brick. Beside the unstable quality, deficiency of synchronal constructing solution besides one of the stand-out issues. Therefore, there was non many building contractors in Vietnam utilizing this edifice stuff. As a consequence, ingestion of AAC is limited, it reached merely around 60-80 % of entire capacity and some fresh-built mills are confronting casual production or menace of bankruptcy. However, harmonizing to non-fired merchandises development plan of the authorities, the premier curate signed the determination that AAC will replace 30-40 % traditional bricks, and it is compulsory for constructing higher than 8 floors. So, with this policy the hereafter of AAC in Vietnam is valuated as brightest among other stuffs.

Table 8: Vietnam AAC Factories production and ingestion in 2012.

| No. | Company | Location in Vietnam | Capacity( m3/year ) | Actual Consumption( M3 ) |

| Entire 9 mills | 1.500.000 | |||

| 1 | Viglacera AAC | Bac Ninh | 200.000 | 150.000 |

| 2 | Vinema | Ha Nam | 100.000 | 60.000 |

| 3 | Song Da Cao Cuong | Hai Duong | 200.000 | 100.000 |

| 4 | Phuc Son | Hoa Binh | 150.000 | 90.000 |

| 5 | An Tai | Phu Tho | 300.000 | 240.000 |

| 6 | Truong Hai | Hai Duong | 200.000 | 110.000 |

| 7 | Vinh Duc | Lam Dong | 100.000 | 50.000 |

| 8 | Vuong Hai | Dong Nai | 100.000 | 60.000 |

| 9 | Ky Nguyen E-block | Long An | 150.000 | 70.000 |

( Vietnam Ministry of Construction, 2013 )

Refering cement market in Vietnam, it has been even worse than other stuffs. Due to authorities policy on take downing rising prices, stabilising market monetary value and macroeconomic, from 2008 to show, cement monetary value merely increased approximately 30 % while input stuffs, coal monetary value raised 4 times. In add-on, electricity, fuel monetary value besides rocketed continuously. Furthermore, from 2010, the exchange rate between VND-USD rose and the entree to banking recognition was hard, so cost over cement monetary value jumped up 20-30 % . Harmonizing to Vietnam Cement Association, entire cost of fabrication is 60 % of selling monetary value, exchange rate increased, loan involvement is approximately 20 % /year, about all cement companies in 2011, 2012, 2013 suffered losingss. For illustration, Cam Pha and Ha Long cement mill had accumulated debt of 1200 billion VND ( about 56 million USD ) and 1090 billion VND ( 51 million USD ) severally.

Reports of Vietnam Cement Association said 48 million dozenss of cement was manufactured in 2012, the figure decreased 5 % compared to that of 2011. Domestic ingestion recorded a figure of 40 million dozenss, about 18 % of diminution. The designed capacity is about 70 million dozenss, but the existent production merely hit 52 million dozenss ( 72 % of capacity ) .

Vietnam steel and metal industry has stayed in the same state of affairs. However, the problems are non merely oversupply caused by frozen building sector, but besides the limited capital, legion debt from loans, natural input ingredients relied on importing beginnings, outdated production engineering. All of those grounds led to weak competitory strength on its ain home-market. Harmonizing to Vietnam steel association’s 2013 study, approximately 30 % of Vietnam steel makers were utilizing old engineering, more than 40 % with mean engineering, and merely less than 30 % of steel houses had new engineering for production and direction. Furthermore, 2013 growing rate was 7 % ; entire capacity reached 10 million dozenss, 8.5 % y-o-y growing but the existent domestic ingestion ill hit 1/3 of capacity.

In drumhead, Vietnamese edifice stuffs companies have been endeavouring to happen solutions to get the better of domestic clang since crisis happened. Although the authorities provided some encouraging actions for the sector since 2011 and so ratified $ 3.3 billion economic bundle in early 2014 ( Dieu Tu Uyen, 2014 ) , the edifice stuffs industry seems to be hard to retrieve. In 2013, there were 10077 building and existent estate companies went bankruptcy, while other houses were fighting in undertaking the oversupply issue.

1.2.3 Export & A ; international concern state of affairs

Due to the troubles of local market, many companies have tried to heighten exporting activity. However, the bulk of merchandises is still chiefly used for devouring inside the state and export’s net incomes could non cover the losingss of domestic sale. It happened to all sort of edifice stuffs.

In general, export turnover of edifice stuffs in 2011 hit somewhat over 766 million USD, that was an 86.45 % addition comparison to 2010. See the tabular array below:

Table 9: Export turnover of edifice stuffs in 2011 and per centum of addition.

| No | Type of edifice stuff | Employee turnover ( thousand USD ) | Percentage of addition ( % ) | |

| 2010 | 2011 | |||

| 1 | Building Stone | 105.646 | 131.715 | 24.67 |

| 2 | Tiles | 109.656 | 185.144 | 68.84 |

| 3 | Sanitary ware | 46.481 | 64.343 | 38.42 |

| 4 | Glass | 40.135 | 49.027 | 22.15 |

| 5 | Clinker and cement | 96.887 | 319.101 | 229.35 |

| 6 | Natural stuffs | 12.027 | 16.682 | 38.70 |

| Entire | 410.832 | 766.012 | 86.45 | |

Sing edifice rocks, top 10 companies accounted for more than 66 % of entire exporting gross of rock. The top consuming markets of Vietnam rock are Belgium ( 29.21 % ) , Australia ( 13.38 % ) and United States ( 9 % ) .

Mentioning to ceramic merchandises, merely about 15 % of entire manufactured goods was exported. Top 10 companies constituted 56 % of entire gross, and the biggest markets are Laos, Taiwan, Thailand, Cambodia, etc. Besides that, tiles and healthful ware have been imported with lower monetary value than Vietnamese houses, most of them come from China. It has pushed domestic makers to confront high force per unit areas and challenges in selling merchandises in the state market.

Table 10: Import and Export state of affairs of tiles and healthful of Vietnam.

| Consumption | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | |

| Export ( million USD ) | Tiles | 77.16 | 80.88 | 69.57 | 109.66 | 185.14 | 190 |

| Sanitary ware | 35.7 | 41.3 | 37.4 | 46.5 | 64.3 | 65 | |

| Import ( million USD ) | Tiles | 33.65 | 22.4 | 70.16 | 95.5 | 46.4 | 46 |

| Sanitary ware | 4.2 | 6.8 | 6.7 | 8.07 | 12.54 | 12 | |

( Vietnam Ceramic Business Association, 2013 )

Harmonizing to top exporting states of ceramic tiles, Vietnam was ranked the 12Thursdaywith 28 million square metre exported in 2010, that accounted for 0.3 % and 1.5 % on the universe ingestion and the universe export severally ( Stock, 2010 ) . However, in footings of money, the entire value of exported tiles of Vietnam is much lower than Thailand and Malaysia ( non mentioned China here ) . The Vietnam Association for Building stuffs A said that the ground is because the competitory strength of Vietnamese houses is lower than Thailand, Malaysia, and China.

Sing to glaze, entire value of glass and glass related merchandises was $ 0.54 billion in 2012. It was a 46.7 % rise comparison to 2011. However, because of the domestic downswing, this addition could non cover the loss in glass sector. For illustration, Mr. Nguyen Anh Tuan said in the interview that Viglacera Corporation still had to shut their glass mill in the North for more than 12 months in malice of holding foreign clients.

About cement sector, in the last 10 old ages, Vietnam cement by and large had the lower merchandising monetary value than other states in ASEAN. It stayed at around $ 50/ton, while the ASEAN mean cement monetary value fluctuated from $ 65 to $ 75/ton ( Vietnam National Cement Association, 2013 ) . In 2012, exporting volume levelled up to 1.7 million dozenss of cement and 7.3 million dozenss of cinder. After that, in 2013, entire cement and cinder exported increased to about 14 million dozenss. This was a large spring in Vietnam cement industry on international concern.

It is clearly seen that constructing stuffs merchandises such as tiles, healthful ware, glass, cement, or steel have had a stable addition in export. However, these betterments could non assist to get the better of the downward tendency in domestic market. Harmonizing to edifice stuffs concern community, the ASEAN market is considered as similarities and has strong points for Vietnamese companies to spread out concerns. So, most of edifice stuffs makers in Vietnam has focused largely on this countries. The imposed revenue enhancement for goods from Vietnam is 0 % , but the proficient barrier and quality is extremely required. Particularly, ASEAN states besides purely control and use the anti-dumping policies. Together with the competition with China, it makes the net incomes of exports stay comparatively little.

However, if Vietnam succeeds in subscribing the Trans-Pacific Partnership understanding, Vietnamese houses will hold greater opportunities to spread out their concern into different states outside ASEAN. Currently, Vietnam companies are paying import revenue enhancement for members of TPP such as Mexico 25 % , Chile 6 % , Peru 5 % , etc. Therefore, when Vietnam joins TPP, import revenue enhancement peers 0 % , companies will hold more inducements to work these possible markets. This besides true for other trade understandings Vietnam is negociating.

1.3 Decision

The fiscal crisis did hold an highly negative impact on building and edifice stuffs industry. Factories had to cut down their capacity around 30 % in general. The goods in stock increased and was hard to sell, particularly for tiles sector. Many companies went insolvents, some have to shut their mills, and many of them suffered losingss.

The export volume and value of constructing stuffs merchandises have kept lifting recent old ages. However it can non cover the immense losingss in domestic market.

On the other manus, the state-owned endeavors have dominated the sector over the private companies.